Since the V’18 expiry the sugar market has rallied strongly, London Sugar Week showed most people are no longer bearish. Is the sugar market surplus really over? [2,650 words/13 minutes’ reading time] This article first appeared for paying subscribers last week.

No-One Knows Anything Any More

The most interesting thing we learnt at London Sugar Week 2018 was that most people are no longer bearish. Perhaps this isn’t surprising. The No.11 market is more than 30% higher than the recent lows. After weeks of waiting for news on Indian subsidised exports, speculative short positions have been covered. We also didn’t meet anyone who was bullish, so it seems people are looking for direction.

We remain negative on price. We struggle to see why raw sugar prices should approach 15c again. If anything we think they should be closer to 10c. Global sugar stocks are the highest they’ve ever been. We also think that it is easy to understate how difficult it will be for India to export 5m tonnes of sugar when world sugar stocks are this high. We’re talking about increasing global sugar supply by 10%, but we don’t actually need a single additional tonne.

Higher prices also risk locking in sugar production that is not needed. To examine this in more detail, we have decided to look at the problem of sugar overproduction. Have producers changed their behaviour? Was 10c enough to resolve the sugar surplus?

There is Too Much Sugar

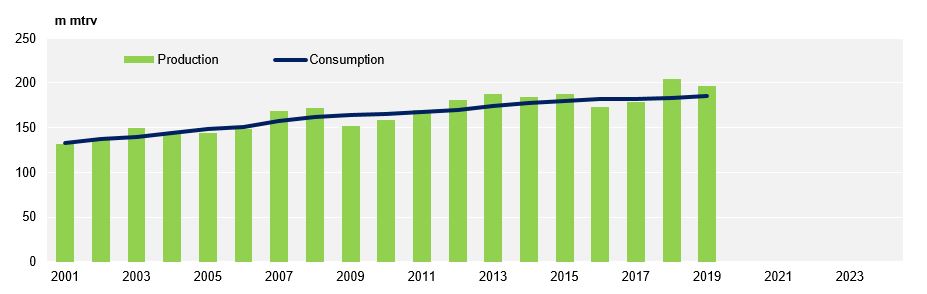

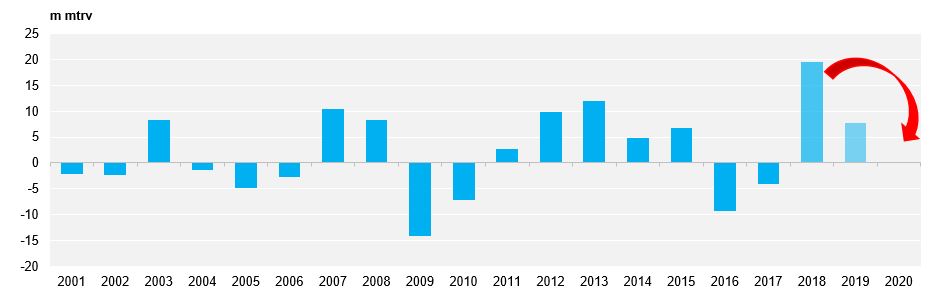

In the 2017/18 season, global sugar production exceeded 200m tonnes (raw value) for the first time. For the 2018/19 season that’s just begun we think production will remain close to this level.

Global Sugar Production Has Hit 200m Tonnes (RV)

This poses a problem. If production remains at 200m tonnes it’s going to take consumption 6 years to catch up. If we are to avoid building sugar stocks to 2024, we need to see someone respond to lower prices and change behaviour. Who?

Does This Mean 6 More Years of Surplus?

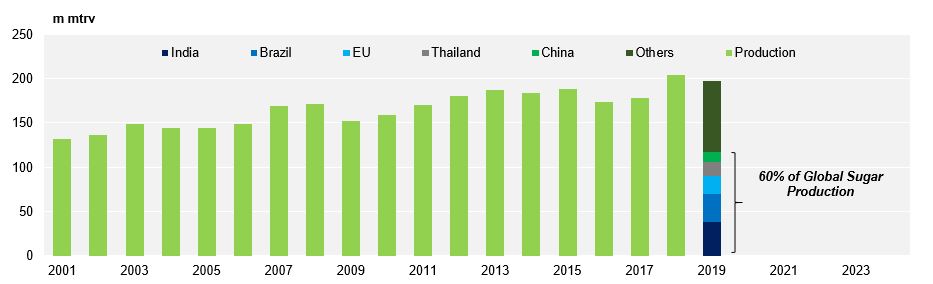

Sugar production is dominated by a handful of countries, so it makes sense to concentrate on these. The major producers of sugar are India, Centre-South Brazil, the EU, NAFTA (now called USMCA), Thailand, and China.

In Which Countries Might Behaviour Change?

We’re going to leave USMCA to one side; its interaction with the world market is small. We can split the remaining countries into two categories: countries where farmers are unlikely to switch from sugar cane growth and countries where farmers’ planting decisions will be important.

India

Let’s start with a blunt statement: it’s difficult to see why Indian cane area should shrink.

Cane prices are set by the government. They are set at a level which gives farmers a good return. The reason is political. Cane farmers are an important source of votes in sugar cane regions in the north and west of the country. In addition, the mills where the farmers’ cane is crushed are often owned by politicians or aspiring politicians.

India – Cane Returns are Excellent

The relationship between the mills/politicians and the farmers runs into difficulty when mills can’t afford to pay farmers on time for their cane. This typically happens in surplus seasons when sugar prices are too low to make cane payments. However, presently the ex-mill sugar price is fixed close to cost of production. While mills are definitely struggling, especially given working capital requirements ahead of the start of cane processing in November, cane arrears are below where they would otherwise be.

As well as fixing the domestic price the government is clearly doing everything it can to support payments to the farmer, including a cane subsidy and a sugar transport subsidy for export. These are likely to be challenged at the WTO by other sugar producers in the coming weeks. However, the level of government support to the farmer means it’s very unlikely cane prices will fall in the coming years. Farmers will therefore continue to grow cane and acreage is therefore unlikely to fall. Indian sucrose output is therefore in the hands of the weather.

This means we’re locked into producing a certain amount of sucrose, equivalent to more than 30m tonnes of sugar indefinitely. This will ensure India remains in surplus for the foreseeable future, which isn’t good news.

The Indian government has recognised that overproduction of sugar won’t go away. If they won’t link cane and sugar prices and can’t reliably (or profitably) export, then sugar stocks will continue to build in India, creating a financial burden for the government. As a result, the government is looking at how to manage this problem.

As Brazil shows, sugarcane is an energy crop. India imports almost all of its liquid transport fuels. When oil prices are high and the Rupee is low this puts pressure on the economy. Making more ethanol from cane is one way to relieve this pressure, while also increasing energy security.

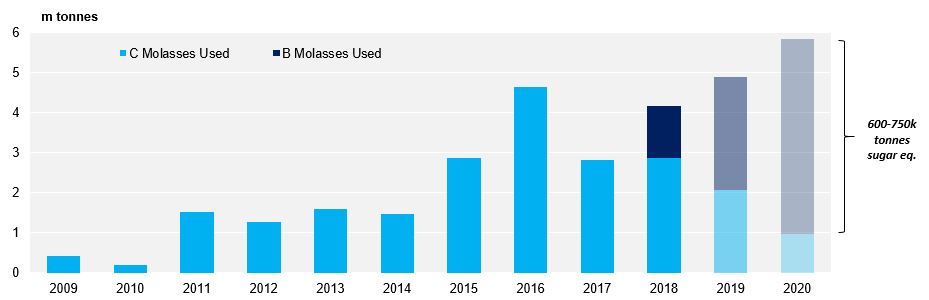

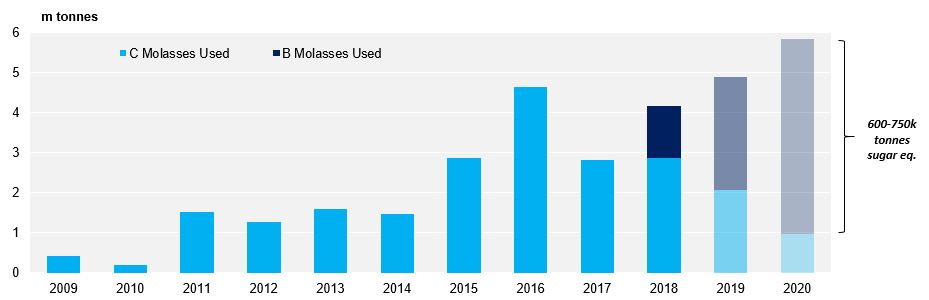

India already has a 5% ethanol mandate, which has never been met. Differences in taxation across states have made it difficult to move ethanol around the country, which has made it hard for oil companies to procure what they need. They have also frequently been outbid by the potable and industrial ethanol sectors. Meanwhile, mills have only been allowed to make ethanol from low sucrose C Molasses, which is normally otherwise used as animal feed.

This year the government has announced measures to encourage mills to make more ethanol and also to encourage the oil industry to buy it. Mills are now allowed to use higher-sucrose B Molasses to make ethanol. They will also be able to use cane juice directly, as in Brazil, though this is likely to need new investment in distilleries and so won’t be an immediate solution.

Import regulations have been changing too. Ethanol can be imported for potable and industrial use, but can no longer be imported for fuel use. This pushes the oil companies to buy ethanol from sugar mills instead. Finally, ethanol prices have been fixed at levels which make it profitable for mills, especially if they use B Molasses as a feedstock.

India – Move to B Molasses to Make Ethanol Will Reduce Sugar Production

We think this means that India is far more likely to reach its 5% ethanol in gasoline blend target, and that mills will increase their output of ethanol. We are already seeing increased use of B Molasses to make ethanol. We think this will result in 350k tonnes less sugar production this coming season, and perhaps up to 750k tonnes less the following year. Once cane juice distilleries are built, these numbers could grow further.

However, all of these measures are driven by changes to Indian regulations, not by the price of sugar. So we’ll move onto the world’s second largest sugar producer, Centre-South Brazil, to see if price is changing behaviour here.

CS Brazil

Mills in CS Brazil choose whether to make sugar or ethanol based on which gives the best return. For the current season the relative returns have been hugely in favour of ethanol, and mills have responded by diverting the highest proportion of cane juice to ethanol production since 1997.

CS Brazil – Close to Maximum Ethanol Mix

This year has shown us how effective the CS Brazilian mills can be at debottlenecking their ethanol operations. The sector has achieved ethanol output beyond what we thought was possible; we’d originally forecast the ethanol mix at 60%. We think this trend could continue next year. Assuming a normal weather, sugar concentration is likely to be lower, which favours ethanol production. Furthermore, lower cane volumes should allow mills to flex more output to ethanol by slowing down the cane crushing rate. We’ve also heard rumours of more efficient enzymes used in the fermentation process. So we are very tentatively assuming that we could see further sugar lost next season to ethanol production.

This outlook assumes no wild moves in FX, that oil prices remain high and that Petrobras don’t change their existing world-energy-market-linked pricing policy. The second round of voting for the Brazilian presidential elections (28th October) could be a source of volatility in the FX and could lead to a change in Petrobras’ policy depending on the result. Moreover, sugar becomes a more attractive product for the mills again at 15c (based on today’s ethanol prices). If the raw sugar market rallies above this level, we should assume more sugar production in 2019.

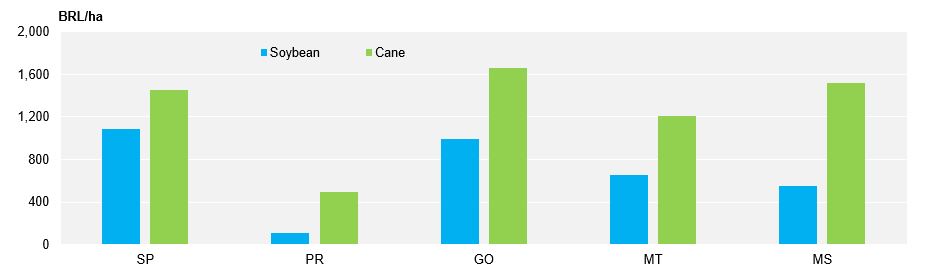

We are also assuming that CS Brazilian cane acreage won’t really change in 2019. It’s worth examining this assumption in a little more detail, particularly given recent news articles that soy is offering some farmers superior returns.

This story sounds credible; No.11 raw sugar prices have been at 10-year lows while Brazilian soybean physical values have benefitted from the USA-China trade dispute and the banning of US soy imports by China.

CS Brazil – Cane Still Favoured

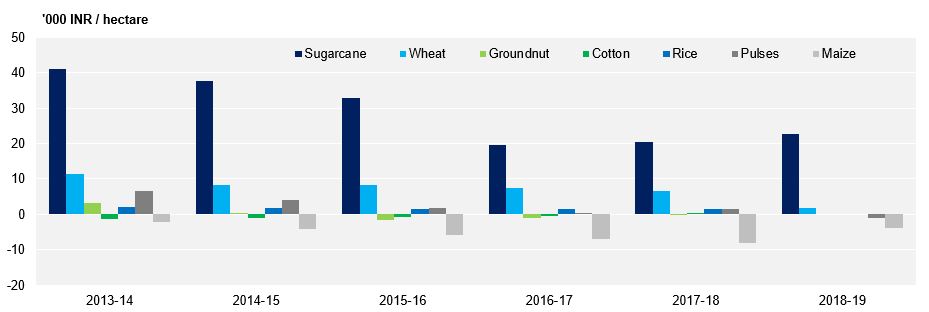

However, we think that we are unlikely to see a meaningful reduction in cane area in CS Brazil. Competition between grains and cane is most pronounced in the frontier states of Goias (GO), Mato Grosso (MT) and Mato Grosso do Sul (MS), not the cane heartlands of Sao Paulo (SP) and Parana (PR). These frontier states also have the highest proportion of mill-owned (not farmer-owned) cane. Sugar mills are unlikely to replace their own cane with other crops because this risks reduced mill throughput, increasing inefficiency and driving up costs relative to output.

We also calculate that for many mills and farmers, cane is competitive versus soy. This is because the Consecana cane formula takes into account ethanol returns as well as domestic and world market sugar returns, and these ethanol returns are positive. Don’t forget that cane is a less intensive crop to grow than soy or corn.

However, third-party cane farmers do have another consideration: the CS Brazilian milling sector is financially distressed, and so farmers aren’t guaranteed to be paid on time or in full for their cane. If cane payments are late or incomplete it is possible we see some farmers divert a little acreage. Another determinant factor is mills closure. If a mill shuts down entirely due to bankruptcy, third-party farmers have to supply cane to a different mill or grow a different crop.

We therefore don’t think CS Brazilian cane acreage will decline significantly in the future. What matters is that the mills continue to operate and continue to maximise ethanol output.

Let’s now look at the next tier of major global sugar producers. In contrast with India and CS Brazil, we believe that current prices are changing farmers’ planting decisions in Europe, Thailand and China.

The EU

European sugar is made from beet, not cane. Beet is an annual crop with a short growing cycle, which means that farmers can respond very quickly to changes in returns.

The European sugar sector was deregulated in October 2017. From this date sugar production and trade were no longer heavily controlled by the European Commission. Many beet processors signed three-year beet supply deals with farmers to ensure resource through this period. These deals were made when the price of sugar was significantly higher than it is today, and so recent farmer returns from beet have been excellent. However, beet processors have done less well as they have faced falling sugar returns.

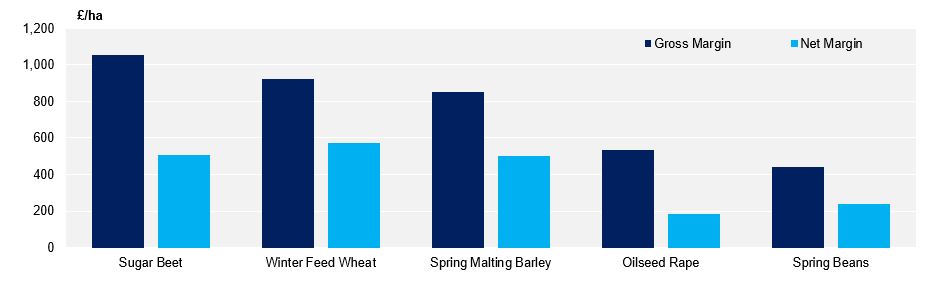

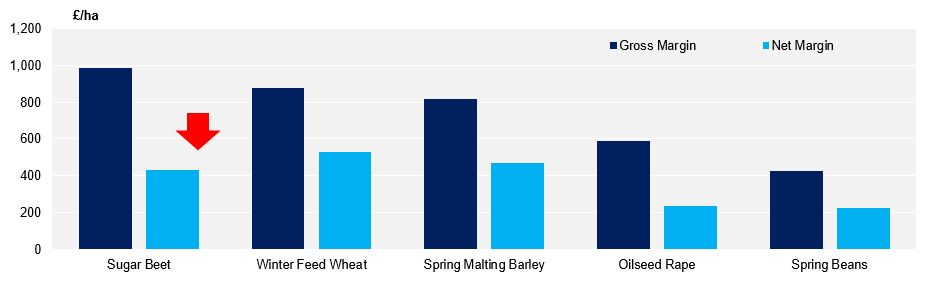

EU – Crop Returns in the Uk in 2018…

This will change in 2019. Three-year beet deals start to expire and the contracts farmers are being offered pay a lot less for beet. For example, we calculate that in the UK in 2018 sugar beet was the crop with the highest gross margin for farmers, and also provided a decent net margin. In 2019, the returns are lower, which might lead to reduced acreage. One reason is that the beet price is going to fall by almost 10%. Another reason is the ban on neonicotinoid pesticides which will come into place. This will probably lead to a drop in yields or an increase in spraying costs.

…And in 2019

European sugar production therefore looks set to fall, and this is unlikely to change until beet processors can offer a higher beet price. This requires an increase in the world sugar market price.

Thailand

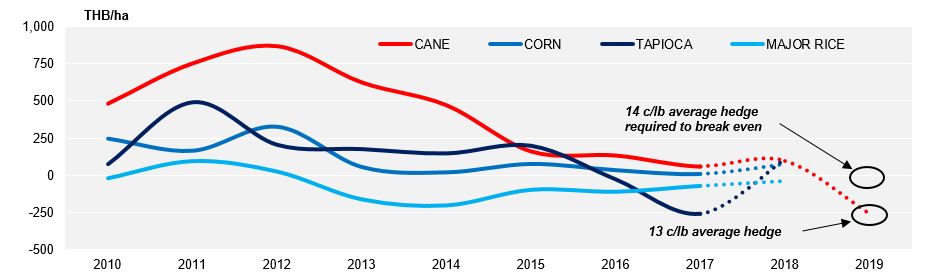

Farmer returns are also under pressure is Thailand. For years sugar cane has been the best returning crop, a consequence of good world market prices and additional support from the government via the Thai Sugar Fund and loans from agricultural banks.

However, world sugar prices have collapsed at the same time as the Thai sugar sector has been reformed under threat from a Brazilian WTO complaint. In the past domestic prices were fixed at profitable levels. Nowadays, they are floating and likely to converge with the world market.

Thailand – Cane Returns Collapse

This means sugar cane is about to become a negative margin crop for many farmers. Cane prices are still driven by the world market hedging levels the Thai Cane and Sugar Corporation achieves. If the TCSC can achieve an average hedge of 13c/lb for 2019, farmers could lose money growing cane. If they can hedge at 14c, farmers will break even. However, crops like cassava and corn are offering better returns today. We are likely to lose cane acreage to other crops unless the world market trades significantly above 14c.

China

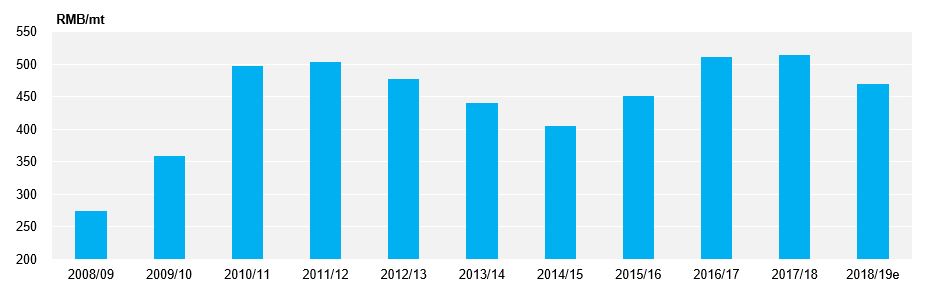

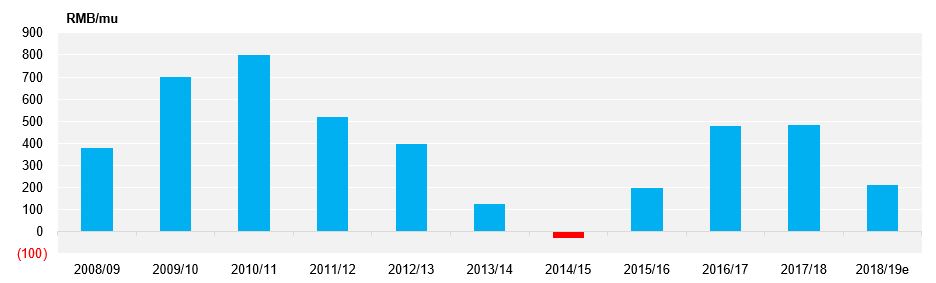

We also believe we will see a reduction in cane acreage in China in 2019, because we expect cane prices fall. However, unlike in Thailand, Chinese cane prices are not linked to the world market. The sugar sector in China is heavily controlled by the government. China is a deficit sugar producer, and imports are restricted. This supports the domestic price at a level far above the cost of production, so farmers can be paid a high price for cane without bankrupting local sugar mills. However, this policy has been undermined by smuggling of sugar into China.

Chinese Cane Prices Look Set To Fall

The scale of the smuggling is huge; it’s one of the largest flows of sugar in the world at around 2.5m tonnes a year. This has forced the government to look at alternative ways to support cane farmers. One proposal is that the government could make direct support payments to farmers and so allow the domestic price to fall. However, direct payments are unlikely to be made before 2020, and so in the short and medium term high domestic prices look set to continue. Meanwhile, local mills are struggling to compete with smugglers. Domestic prices are not high enough to make the milling sector profitable. Mills are therefore campaigning for lower cane prices to help them break even. If cane prices fall, farmers will lose money and we could see either a reduction in cane acreage or an increase in intercropping cane with other crops, such as watermelons.

China – Cane Farmer Returns will More Than Halve

In summary, we don’t expect to see a large decline in Indian or CS Brazilian cane acreage in the coming years. However, we should see beet acreage fall in the EU, and cane acreage retreat in Thailand and China. In addition, ethanol production from cane is likely to grow in importance if oil prices remain high and sugar prices remain low. So perhaps behaviour is starting to change after all. Is this going to be sufficient to move the market back to a deficit?

A Return to Sugar Production Deficit, or Continued Oversupply?

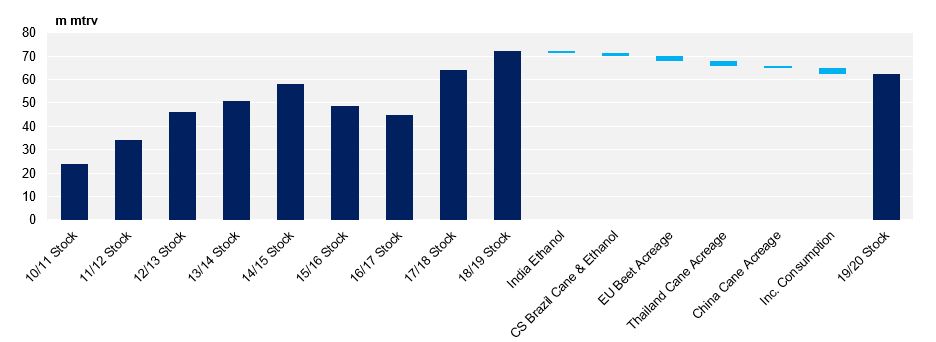

The following chart shows whether the world is producing too much or too little sugar each year. The 2017/18 season had record oversupply. 2018/19 also has a large surplus. This means global sugar stocks are building rapidly, which is one of the reasons sugar prices are so weak.

The Situation Today

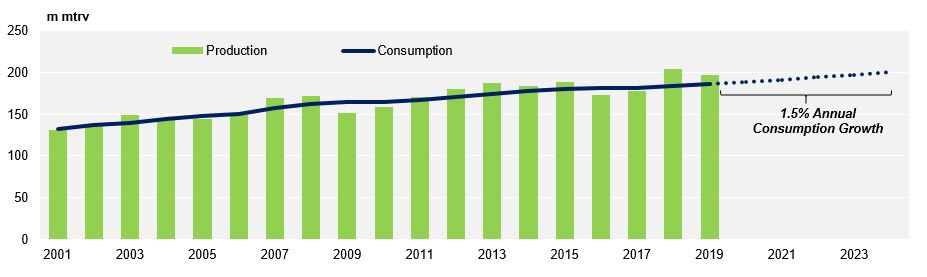

We have had more surplus than deficit years since 2008, and the surpluses are getting larger while the deficits are getting smaller. If we take the 2018/19 stocks and apply all of the changes which we’ve discussed in this report, 2019/20 stocks will remain above the levels seen before this most recent stock build.

2019/20 – Stocks Still High

This outlook is interesting because it suggests we may not add to global sugar stocks in 2020, which is four years sooner than if we’d had to rely on consumption growth alone. However, a balanced market still leaves the problem of what to do with the huge stocks which have built in 2017 and 2018. These stocks will continue to hang over the market in the coming years unless production falls below consumption. For this to happen we need a further event: perhaps poor weather disrupting cane or beet crops, or logistical disruption at a key sugar supplier. Without this, the market will remain weak.